It has been a wild ride for mortgage rates over the past month, which touched record lows then rebounded just as fast. Low rates are typically associated with healthy housing demand and a strong market – especially now that we've entered home shopping season – but early signs indicate the market is slowing.

As the calendar turned and the Federal Reserve made its first of two March interest rate cuts, mortgage rates reached record lows. This sparked a historic flurry of refinancing activity, which jumped as much as 79% in a week and 479% from a year earlier, prompting the Mortgage Bankers Association to double its forecast for refinance originations in 2020.

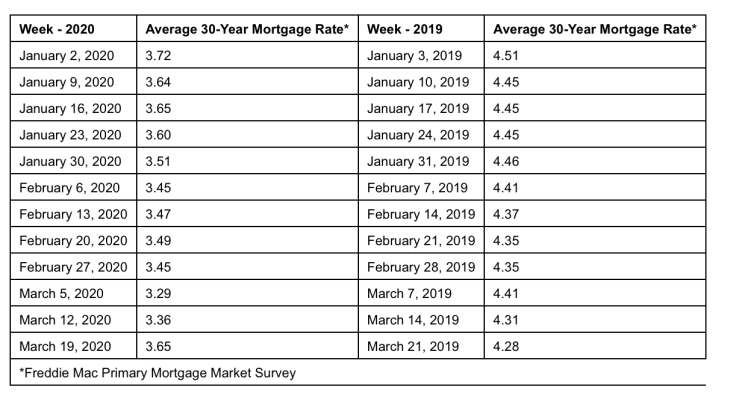

But mortgage rates have jumped sharply in the days since, up a full percentage point since hitting record lows, baffling market observers as they moved counter to other measures such as Treasury yields. Despite these recent gains, rates are still low relative to historic norms, sitting about 60 basis points lower than this time last year.

In a typical market, low mortgage rates would be expected to continue to boost demand -- the most recent reading on home sales in February was strong, suggesting that buying demand remained healthy at the start of the year despite a historic shortage of inventory, in part because of low mortgage rates that make monthly payments more affordable.

But today's market is, of course, anything but typical as some jurisdictions have mandated or recommended citizens remain at home in an effort to slow the spread of COVID-19. The effect these recent mortgage rate movements are having on the housing market has been overshadowed by broader economic factors, and the most prominent impact may have already come to pass with the temporary boom in refinances.

One sign of analysts' reading of the market is Bank of America's ratings downgrade for some of the nation's largest homebuilders, suggesting the bank believes COVID-19 will harm consumer sentiment and slow homebuilding. If correct, that dive in consumer sentiment would presumably slow sales activity regardless of mortgage rate movements as some would-be buyers turn down their risk tolerance and stay out of the market. Early data suggests this may be the case as real estate showings have dropped off steeply since March 11ii.

Recent data on the economy at large have been less than encouraging as well, including a surge in weekly jobless claims. The Federal Housing Administration's decision to implement a 60-day moratorium on foreclosures and evictions for many homeowners reduces the risk of a wave of foreclosures, which would likely drive down home values. There is no indication to this point that home values have been affected by the slowdown.

"The U.S. housing market has entered truly uncharted territory, shaken by the COVID-19 pandemic and a corresponding, sharp economic contraction that has already caused millions of Americans to lose their jobs," said Zillow Economist Jeff Tucker. "Rock-bottom mortgage rates have provided some small financial relief for homeowners and buyers, but it hasn't been enough to avoid a slowdown. The big question at the moment is to what degree measures being taken by local, state and national legislators will help limit the number of foreclosures in the months ahead."

More will be revealed in the coming weeks as this unprecedented situation continues to unfold, and Zillow economists will be closely monitoring each development.

© 2025 Latin Times. All rights reserved. Do not reproduce without permission.